A look at the day ahead in European and global markets

|

|

|

|

By Tom Westbrook, Deputy Financial Markets Editor

|

|

|

|

|

The session is the first buying day for the quarter ahead, given that trades settle the following day.

In the quarter closing out, the biggest oil supply shock on record has hardly left a blemish on financial markets, as demand cuts in China, alternative shipping routes and producers plugged the crude shortfall.

|

|

|

|

Oil retreats, shares gain on AI |

The German share price index DAX graph is pictured at the stock exchange in Frankfurt, Germany, June 29, 2026. REUTERS/staff

|

Oil prices have fallen back to levels before the U.S.-Israeli-Iran conflict began at the end of February, and skirmishes straining the ceasefire are drawing little reaction.

Even the bond market seems to be moving on. Traders are sticking with expectations for modest U.S. rate hikes, though on the basis of strong U.S. growth rather than runaway inflation.

Bonds were mostly unmoved by the U.S. Supreme Court's refusal, as foreshadowed in January, to let President Donald Trump fire Fed governor Lisa Cook.

And the AI rally has run on unhindered, driving gains of 100% in the first half for South Korea's KOSPI index and a record quarterly rise of about 36% for Japan's Nikkei.

Flows have been counterintuitive, with foreign cash streaming out from South Korea and dragging down the won as investors take profit and rebalance through the rally, leaving retail investors to chase the gains.

|

Graphics are produced by Reuters

|

|

|

|

Some recent speed wobbles may turn market focus to a broader range of rising but less red-hot stocks in Europe, where the STOXX index is up about 9% for the quarter, and Asia, where China's mainland blue chips are up 10%.

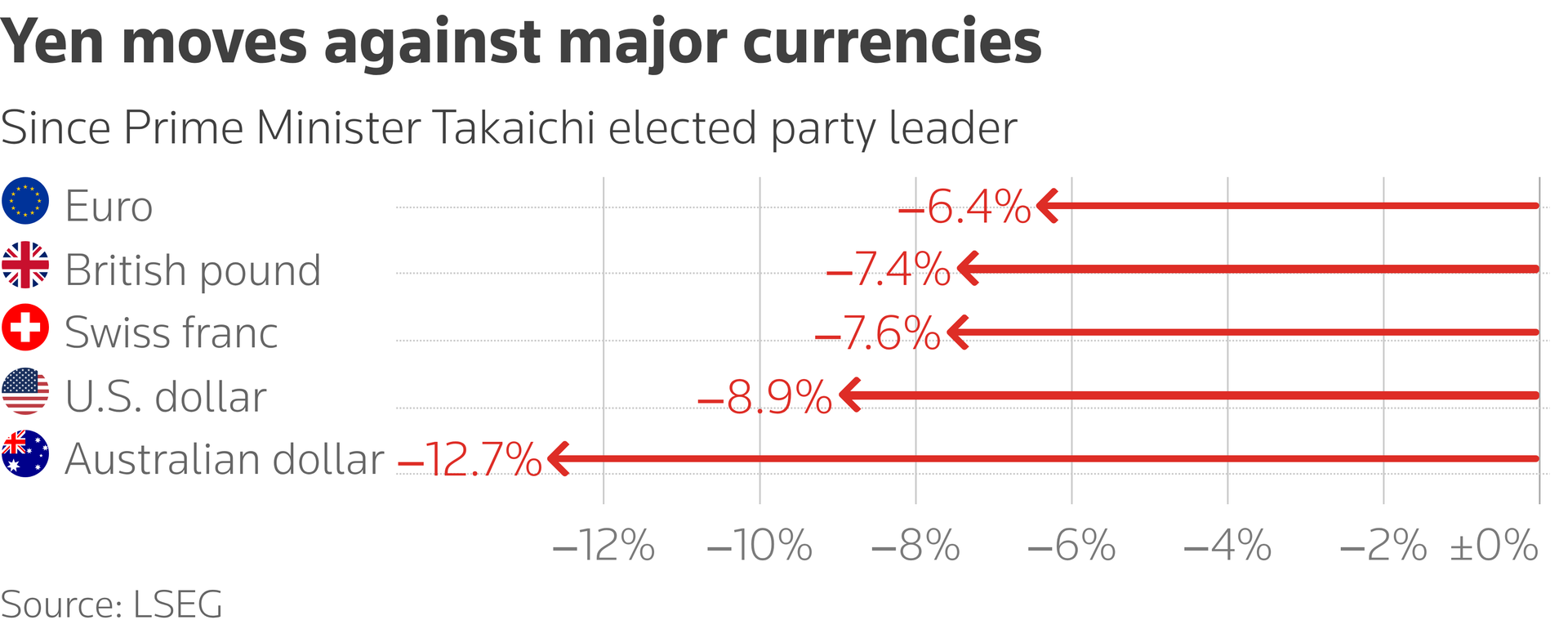

And the yen is on the ropes, along with the won, thanks to the markets' view that Japan is lagging behind a global move higher in interest rates. It crossed 162 to the dollar for the first time since 1986 in the Asia session and the risk of intervention is higher and higher, traders say, the nearer the rate nudges to 165.

German, French and Italian inflation readings are due and could show annual rates dropping and reinforce that rates can be on hold in Europe for some time.

The European Central Bank's Isabel Schnabel appears on a panel in Sintra, where Fed Chair Kevin Warsh is due on Wednesday.

|

|

|

|

Key developments that could influence markets on Tuesday: |

- Economics: European inflation, British GDP, U.S. job openings and consumer confidence

- Events: Sintra Forum

|

|

|

|

Opinions expressed are those of the author. They do not reflect the views of Reuters News, which, under the Trust Principles, is committed to integrity, independence, and freedom from bias.

|

|

|

|

|

|

| |

|

|

Morning Bid is sent every weekday morning. Think your friend or colleague should know about us? Forward this newsletter to them. They can also sign up here. Want to stop receiving this email? Unsubscribe here. To manage which newsletters you're signed up for, click here. This email includes limited tracking for Reuters to understand whether you’ve engaged with its contents. For more information on how we process your personal information and your rights, please see our Privacy Statement. Terms & Conditions |

|

| |

© 2026 Thomson Reuters. All rights reserved.

3 Times Square, New York, NY 10036 |

|

|

|

|

|

No comments:

Post a Comment