A look at the day ahead in European and global markets

|

|

|

|

By Stella Qiu, Australia Economics & Markets Correspondent

|

|

|

|

|

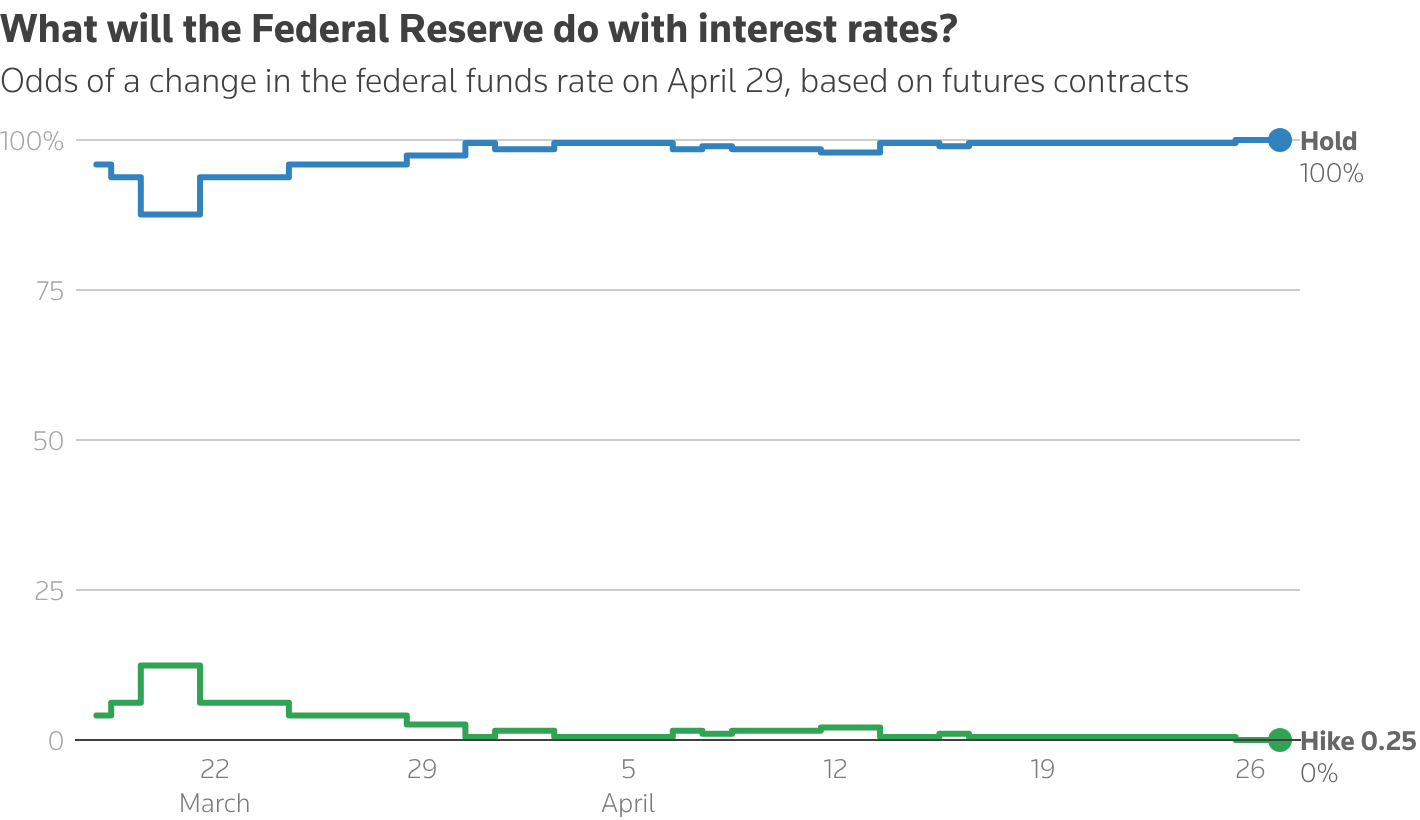

Jerome Powell's parting gift as Fed Chair was a proper hawkish tilt - the U.S. central bank held interest rates steady but in the most divided vote since 1992 three regional presidents dissented over phrasing that pointed to an "easing bias", saying such language was no longer appropriate given elevated inflation and the massive uncertainty about oil prices as a result of the U.S.-backed war against Iran.

|

|

|

|

U.S. Federal Reserve Chair Jerome Powell departs following his final press conference following a two-day meeting of the Federal Open Market Committee (FOMC), at the U.S. Federal Reserve in Washington, D.C., U.S., April 29, 2026. REUTERS/Kevin Lamarque

|

With Brent oil hitting a four-year high of $125 a barrel and the Strait of Hormuz still closed, it is not unusual among central banks - looking at you BoC - to sound the inflation alarm. Media reports say U.S. President Donald Trump will be briefed today on new military options against Iran as peace talks seem to have stalled.

Powell also confirmed he would stay on as a Fed governor until the outlook was clearer, essentially taking the place of Governor Stephen Miran, a Trump loyalist who voted for a rate cut on Wednesday. Many analysts suspect Powell could join the hawks to try and ward off further attempts by Trump and his new Fed Chair Kevin Warsh to lower interest rates.

Fed developments and the jump in oil sent Treasury yields spiking as traders priced out any chance of rate cuts this year. They now see a roughly even chance of a rate hike from the Fed by April 2027. Quite a reversal from before the war began at the end of February.

|

Graphics are produced by Reuters

|

|

|

|

Macro fears, micro euphoria |

Equities, however, were in their own AI-generated world. Nasdaq futures rose around 0.4%, helped by generally positive first-quarter earnings from four tech giants.

Google parent Alphabet soared 7% in extended trade after smashing forecasts. Microsoft and Amazon.com delivered as well, but Meta Platforms disappointed on concerns over its AI spending. All eyes are now on Apple to keep the good times rolling later today.

South Korea's KOSPI was set for a 32% surge in April, the biggest monthly rise since 1998, and Taiwan stocks for a 24.5% gain over the month, the biggest since 2001. Who says there's a war going on?

The gulf between macro fears and micro euphoria sets up a weak European open, with pan-region stock futures down 0.4%. Investors are nervously eyeing the European Central Bank and Bank of England, both due to announce decisions later, fearing they might turn yet more hawkish.

March inflation data from Europe and the U.S. are also due and will reveal the initial impact from the Iran war. A spike in headline inflation is almost certain on higher petrol prices, but everyone knows the worst is yet to come.

|

|

|

|

Key developments that could influence markets on Thursday: |

- Advance estimates for euro zone, U.S. GDP for Q1

- EU inflation for March

- U.S. PCE inflation and spending for March

- ECB and BOE decisions

- Apple Q1 earnings

|

|

|

|

Opinions expressed are those of the author. They do not reflect the views of Reuters News, which, under the Trust Principles, is committed to integrity, independence, and freedom from bias.

|

|

|

|

|

|

| |

|

|

Morning Bid is sent every weekday morning. Think your friend or colleague should know about us? Forward this newsletter to them. They can also sign up here. Want to stop receiving this email? Unsubscribe here. To manage which newsletters you're signed up for, click here. This email includes limited tracking for Reuters to understand whether you’ve engaged with its contents. For more information on how we process your personal information and your rights, please see our Privacy Statement. Terms & Conditions |

|

| |

© 2026 Thomson Reuters. All rights reserved.

3 Times Square, New York, NY 10036 |

|

|

|

|

|

No comments:

Post a Comment